The AEC Lens Alex Carrick, Chief Economist at ConstructConnect

Alex Carrick is Chief Economist for ConstructConnect. He is a frequent contributor to the Daily Commercial News and the Journal of Commerce. He has delivered presentations throughout North America on the Canadian, United States and world construction outlooks. A trusted and often-quoted source for … More » Top 25 U.S. Cities for Medical Facility Construction StartsFebruary 12th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect There are 51 metropolitan statistical areas (CMAs) in the United States with population levels above one million each. Drawing from ConstructConnect’s data pool for those 51 cities, Table 1 ranks the Top 25 markets in America for medical facility construction starts in 2018. (Map 1 showcases the Top 20.) Leading all cities last year was Washington, D.C., with groundbreakings on hospitals, clinics, nursing and seniors’ homes combined valued at $1.3 billion. Next in line were Cleveland ($1.1 billion), Phoenix ($883 million), Cincinnati ($858 million), Pittsburgh ($740 million), Atlanta and Orlando (tied at $736 million), Tampa-St. Petersburg ($718 million); and Houston ($708 million). Notice the presence of a pair of cities in Ohio – i.e., Cleveland and Cincinnati – only a rung or two short of the summit in the dollar-volume listing. Read the rest of Top 25 U.S. Cities for Medical Facility Construction Starts Top 25 U.S. Cities for School Construction StartsFebruary 6th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect There are 51 metropolitan statistical areas (CMAs) in the United States with population levels above one million. Drawing from ConstructConnect’s data pool for those 51 cities, Table 1 ranks the Top 25 markets in America for educational facility construction starts last year. (Map 1 showcases the Top 20.)

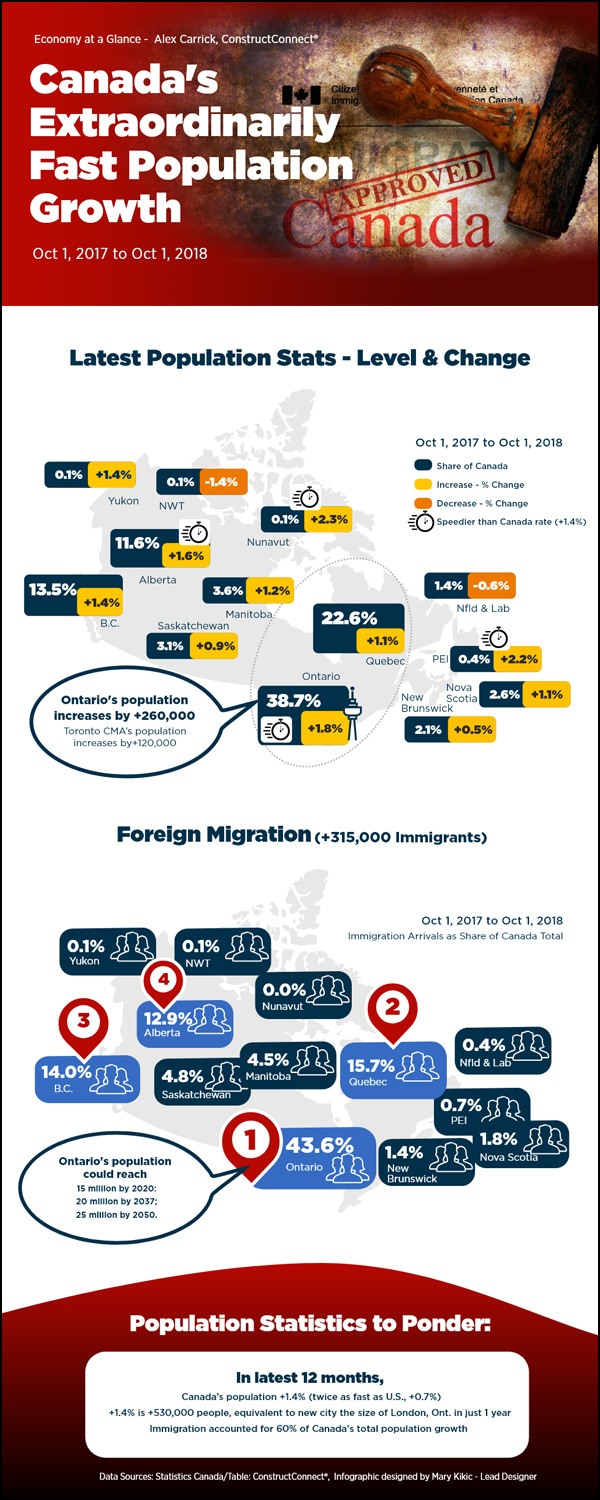

Read the rest of Top 25 U.S. Cities for School Construction Starts Infographic: Canada’s Fast Population GrowthFebruary 1st, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Due to its complexity, much of the subject matter concerning the economy requires detailed editorial commentary, often supported by relevant tables and graphs. This infographic looks at Canada’s extraordinarily fast population growth and the latest statistics.

At the same time, though, there are many topics (e.g., relating to demographics, housing starts, etc.) that cry out for compelling ‘short-hand’ visualizations. Whichever path is followed, the point of the journey, almost always, is to reach a bottom line or two. To provide additional value at its corporate blog site, ConstructConnect is now pleased to offer an ongoing series of Infographics. These will help readers sort out the ‘big picture’ more clearly. Click Here to view the latest infographic. To view more infographics, Click Here Also read the related article, “15 Bullet Points on Canada’s Extraordinarily Fast Population Growth“. 15 Bullet Points on Canada’s Extraordinarily Fast Population GrowthJanuary 28th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect Statistics Canada’s latest national and provincial/territorial population estimates are for October 1, 2019. The two tables included with this article and the 15 bullet points below throw a spotlight on many of Canada’s most recent demographic highlights.

Ramifications of U.S. Shutdown Ripple outwards to China and CanadaJanuary 25th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect U.S. Census Bureau workers are off the job due to Washington’s partial funding shutdown. As a result, current statistics on housing starts, retail purchases and foreign trade are not available. This is no minor matter. It will be difficult to accurately calculate national output – i.e., the important gross domestic product (GDP) measure – without reliable data on many of its key components. GDP growth, or lack thereof, is one key determinant of Federal Reserve interest rate moves. The Fed will struggle over whether to be ‘hawkish’, ‘dovish’, or stick with neutral. Furthermore, the ramifications of economic data omissions are not solely limited to the U.S. The U.S. and China are engaged in a trade skirmish, with tariffs on Chinese goods entering the U.S. slated to increase to 25% from 10% at the end of March, if there is no resolution. The U.S. has been running a huge trade deficit with China for years. In many months, it has been in a range of 40% to 50% of the total U.S. merchandise trade shortfall with all nations. Series (5 of 7): Rankings of States by Industrial Subsector Jobs – Computer Systems DesignJanuary 24th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect

Construction spending in various type-of structure categories is driven by economic circumstances within specific industrial subsectors. For example, manufacturers set the pace in industrial construction.

This article is the fifth in a series of seven that examines key industrial sectors to determine where they are most prominent regionally. Rankings of state strength in each industrial subsector are based on both ‘weight’ and ‘concentration’ of relevant employment. ‘Weight’ is simply the number of jobs in the industrial subsector in each state. ‘Concentration’ is each state’s number of jobs in the subsector divided by the state’s population. In effect, it’s a ‘per capita’ figure, except that it’s expressed as number of jobs per million population. By ‘weight,’ the states with the largest populations are almost always high in the rankings. The rankings by ‘concentration,’ however, often deliver a jolt of surprise or two. Series (4 of 7): Rankings of States by Industrial Subsector Jobs – Leisure and HospitalityJanuary 22nd, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect

Construction spending in various type-of structure categories is driven by economic circumstances within specific industrial subsectors. For example, manufacturers set the pace in industrial construction.

Good health in the leisure and hospitality sector provides the backing for new hotel and motel work. And jobs levels in information and financial services, as well as in more rapidly expanding fields of endeavor such as computer systems and design services, establish the need for additional office space and commercial tower square footage. (See, “Shifts in Office Jobs and Implications for Commercial Tower Construction“.) This article is the fourth in a series of seven that examines key industrial sectors to determine where they are most prominent regionally. Rankings of state strength in each industrial subsector are based on both ‘weight’ and ‘concentration’ of relevant employment. ‘Weight’ is simply the number of jobs in the industrial subsector in each state. ‘Concentration’ is each state’s number of jobs in the subsector divided by the state’s population. In effect, it’s a ‘per capita’ figure, except that it’s expressed as number of jobs per million population. By ‘weight,’ the states with the largest populations are almost always high in the rankings. The rankings by ‘concentration,’ however, often deliver a jolt of surprise or two. State Tiers: It’s important to know that three clear groupings of states emerge from an analysis of the Census Bureau’s latest (i.e., through July 1, 2018) population statistics. Those groupings are: (A) the four frontrunner states by nominal levels of population – California, Texas, Florida, and New York; (B) the three states with the fastest year-over-year gains in population – Nevada, Idaho, and Utah; and (C) another tier of six states with both strong nominal increases and percentage changes in resident counts over the past several years – Washington, North Carolina, Georgia, Arizona, Colorado, and South Carolina. (See, “Latest State Population Statistics, Maps, & Tables – Six Dark Horse Winners.”) Also read, “Series (1 of 7): Rankings of States by Industrial Subsector Jobs – Manufacturing,” “Series (2 of 7): Rankings of States by Industrial Subsector Jobs – Financial Services,” and “Series (3 of 7): Rankings of States by Industrial Subsector Jobs – Information Services.” Series (3 of 7): Rankings of States by Industrial Subsector Jobs – Information ServicesJanuary 18th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect Construction spending in various type-of structure categories is driven by economic circumstances within specific industrial subsectors. For example, manufacturers set the pace in industrial construction.

Good health in the leisure and hospitality sector provides the backing for new hotel and motel work. And jobs levels in information and financial services, as well as in more rapidly expanding fields of endeavor such as computer systems and design services, establish the need for additional office space and commercial tower square footage. (See, “Shifts in Office Jobs and Implications for Commercial Tower Construction.”) This article is the second in a series of seven that examines key industrial sectors to determine where they are most prominent regionally. Rankings of state strength in each industrial subsector are based on both ‘weight’ and ‘concentration’ of relevant employment. ‘Weight’ is simply the number of jobs in the industrial subsector in each state. ‘Concentration’ is each state’s number of jobs in the subsector divided by the state’s population. In effect, it’s a ‘per capita’ figure, except that it’s expressed as number of jobs per million population. By ‘weight’, the states with the largest populations are almost always high in the rankings. The rankings by ‘concentration’, however, often deliver a jolt of surprise or two. Infographic: U.S. Large Project Starts – High-Tech Data Centers and HotelsJanuary 17th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect Due to its complexity, much of the subject matter concerning the economy requires detailed editorial commentary, often supported by relevant tables and graphs. This infographic looks at U.S. large project starts in high-tech data and fulfillment centers and hotels and conference centers.

At the same time, though, there are many topics (e.g., relating to demographics, housing starts, etc.) that cry out for compelling ‘short-hand’ visualizations. Whichever path is followed, the point of the journey, almost always, is to reach a bottom line or two. To provide additional value at its corporate blog site, ConstructConnect is now pleased to offer an ongoing series of Infographics. These will help readers sort out the ‘big picture’ more clearly. To view the latest infographic.

8 Mid-January Economic NuggetsJanuary 17th, 2019 by Alex Carrick, Chief Economist at ConstructConnect

Article source: ConstructConnect Well this is a fine pickle, I must say. I’m about to try writing a Nuggets report based on the latest statistical releases and many of the U.S. economy’s key data series have not been updated due to the federal government shutdown. Workers at the Bureau of Labor Statistics (BLS), which compiles jobs numbers and inflation rate figures, are still toiling away. But workers with the Census Bureau, which monitors foreign and retail trade, plus housing starts, are off the job.

The number of individuals employed by Washington on a normal workday is a little less than three million. Of that total, and with their paychecks being withheld, 800,000 are now staying at home or working for free. The figure grows considerably larger when sidelined contract workers are included in the tally. To date, this is taking a minor toll on consumer spending, but the impact will become more onerous the longer the stalemate between the President and the House lasts. Prior to recent developments, the story concerning government employment has been largely snooze-inducing. The three levels of government employment – federal, state and local − account for 22.4 million jobs in total. The shares provided by each level have stayed relatively constant over the past ten years. Almost two-thirds (64.5%) of such workers are at the local level; almost one-quarter (23.0%) at the state level; and the remaining 12.5% at the federal level. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||

|

|

|||||

|

|||||

Animation, 3D Art and 3D Models")

{kind=link}