Posts Tagged ‘Economic’

Monday, September 30th, 2019

Article source: ConstructConnect

The U.S. economic recovery and expansion has now lasted more than a decade, which is historically ‘long in the tooth.’ With each passing month, and despite how well the major stock market indices may be doing, worries about a slowdown or next recession become harder to suppress.

The following are some of the yellow flags pointing to potholes in the road ahead. When warranted, countervailing positives have been added.

(1) Running Out of Track for the Stimulus Train

At present, it’s the absence of something special to look forward to that is significant. Heading into 2018, executives throughout the U.S. were eagerly anticipating the steep cut in the corporate tax rate, from 35% to 21%, and several other business-friendly initiatives (i.e., incentives to repatriate money from overseas, etc.). There’s nothing implying a similar upbeat impact on the horizon today.

The Trump administration has floated the idea of a big middle-class income tax cut. A formidable stumbling block, however, has emerged. The estimated federal deficit in the current fiscal year, made worse by the corporate tax cut, will reach -$1 trillion. Washington’s total debt is -$22 trillion and climbing. Personal income tax relief would most likely further exacerbate an already troubling situation.

(more…)

Tags: Alex Carrick, brexit, capex, Deficit, Economic, Economics, Economist, Economy, geopolitical, interest rate, jobs, Labor, population drop, stimulus, Weather

Comments Off on 13 Yellow Flags ‒ Warning Signs Concerning the U.S. Economy

Tuesday, August 6th, 2019

Article source: ConstructConnect

Fed Becomes Erratic in Response to Unorthodox Economic Policy

After achieving +3.1% GDP growth in Q1, the U.S. economy stayed healthy in Q2 at +2.1%. In July, according to the latest ‘Employment Situation’ report from the Bureau of Labor Statistics (BLS), +164,000 net jobs were created in America, on top of a +193,000 gain the month before.

The unemployment rate continues to sit at an exceptionally low 3.7%. Inflation is a little less than +2.0% year over year. All in all, the U.S. economy is in extraordinarily good shape.

How is the Federal Reserve responding? It just lowered its key policy-setting interest rate by 25 basis points (100 bps = 1.00%). It has also suggested that further cuts are no sure thing.

Orthodox economic policy would see a strong U.S. economy raising other economies around the world. Orthodox policy would permit relatively free ‘goods’ flows internationally, resulting in better global trade and heightened demand for commodities. A ‘rising tide would lift all boats’.

(more…)

Tags: Alex Carrick, ConstructConnect, Economic, Economic policy, Economics, Economist, Economy, Growth

Comments Off on U.S. Strong Jobs Growth in July Underlines Fed’s Erratic Interest Rate Move

Thursday, July 18th, 2019

Chinese Economic Slowdown

China’s latest quarter-over-quarter ‘real’ (i.e., after adjustment for inflation) gross domestic product (GDP) growth rate was its slowest since 1992. 2019’s second quarter advance, annualized, was only +6.2%. That level of increase anywhere else in the world would be greeted with celebration, but for China, it’s a relative crawl. While the +10% to +12% gains of the mid-00s have become a thing of the past, +7% or more has still been commonplace in the Middle Kingdom of late. The Chinese economy would greatly benefit from an end to its trade dispute with the U.S. which has seen sales to American consumers significantly curtailed by tariffs.

Meanwhile U.S. Economy Roars

At least with respect to employment, the U.S. economy continues to roar. One of the best indicators of the strength in the jobs market is the ‘weekly initial jobless claims’ data series. It measures first-time applications for unemployment insurance. The figure soars when the economy sinks. As Graph 1 shows, initial jobless claims in the middle of the 2008-2009 recession skyrocketed to 665,000. But they have now been less than 300,000 – i.e., the benchmark usually adopted to denote a solid jobs recovery – for 226 weeks in a row (i.e., more than four years). They even dropped below 200,000 twice in April of this year.

The length of time from high to low in the initial jobless claims curve has been 10 years, exactly corresponding with the duration of the current upbeat economic cycle. When searching for an early warning sign that the economy is faltering, be wary of initial jobless claims rising back to 300,000.

(more…)

Tags: Alex Carrick, China, ConstructConnect, Economic, Economist, employment, Growth, Housing, market, material, money

Comments Off on 7 Mid-July Economic Nuggets, With Emphasis on Jobs Markets

Monday, May 13th, 2019

Article source: ConstructConnect

Total U.S. put-in-place construction spending, after increasing steadily (although slowly) for seven years, from 2011 through 2017, has lost upwards momentum over the past year and a bit. The cause of the overall weakness has been a retreating residential sector. Nonresidential has continued to exhibit a decent degree of uplift.

For various type-of-structure categories of construction, the charts in this article showcase three data sets – (1) seasonally adjusted (SA) monthly ‘current’ dollar volume levels (where ‘current’ means not adjusted for inflation); (2) month-to-month percent changes in the dollar volume; and (3) year-over-year percent changes in the dollar volume.

As shown in Graph 1 below, total spending on U.S. construction reached its zenith in May of last year, at $1.324 trillion. Since that peak, it has fallen by 3.2%, to land at $1.282 trillion in the latest month for which data is available, March 2019.

The average of month-to-month percent changes for total U.S. put-in-place construction spending during the past ten years has been +0.4%. In March 2019, the month-over-month figure was in negative territory, at -0.9%.

Over the past 10 years, the average of year-over-year percent changes recorded each month for total put-in-place construction has been +4.2%. In March 2019, the year-over-year change was -0.8%.

The ‘glory days’ for U.S. put-in-place construction have, for the moment at least, receded.

Total put-in-place construction was doing its best between 2012 and early 2017, when the y/y percent change curve was consistently above the 10-year average line, as seen in the lower portion of Graph 1. Recently, U.S. put-in-place construction has fallen off its earlier faster pace.

(more…)

Tags: Alex Carrick, CMDGroup, Construction industry, Economic, employment, Growth, highway, home, hotel, manufacturing, Motel, residential, street

Comments Off on U.S. Put-in-place Construction Spending Hits a Soft Spot

Thursday, March 7th, 2019

Article source: ConstructConnect

Issuance of year-end data on U.S. new homebuilding activity was delayed due to the partial government shutdown which kept Census Bureau workers away from their desks.

Over the past month, however, there have been diligent catch-up efforts and December’s preliminary residential ‘starts’ and ‘permits’ numbers are now available.

There are ‘starts’ at the national level; but for states and cities, the figures are based on building permits.

This article will mainly concentrate on new home groundbreakings in America’s largest metropolitan statistical areas (MSAs). ‘Permits’ in units will be accepted as equivalent to ‘starts’.

‘Permits’ are first published by the Census Bureau, then repackaged in a more user-friendly form by the National Association of Home Builders (NAHB).

When Canadian statistics are mentioned, they have been made available by Canada Mortgage and Housing Corporation (CMHC) and they are ‘starts’.

(more…)

Tags: Alex Carrick, atlanta, Austin, Canada, Charlotte, chicago, ConstructConnect, Construction industry, Denver, Economic, employment, Houston, los angeles, Miami-Ft Lauderdale, minneapolis-St paul, MSA, nashville, New york, orlando, phoenix, residential, san francisco, seatttle, Tampa, washington DC

Comments Off on 2018 Residential Construction Market Highlights − U.S. and Canada

Friday, February 22nd, 2019

Article source: ConstructConnect

This article is the seventh, or final one, in a series of seven that examines key industrial sectors to determine where they are most significant regionally. Rankings of state strength in each industrial sub-sector are based on both ‘weight’ and ‘concentration’ of relevant employment.

‘Weight’ is simply the number of jobs in the industrial sub-sector in each state. ‘Concentration’ is each state’s number of jobs in the sub-sector divided by the state’s population. In effect, it’s a ‘per capita’ figure, except that it’s expressed as number of jobs per million population.

By ‘weight’, the states with the largest populations are almost always high in the rankings. The rankings by ‘concentration’, however, often expose some unexpected winners.

(more…)

Tags: Alex Carrick, ConstructConnect, Economic, Economics, Growth, home, Housing, interest rate, job, money

Comments Off on Series (7 of 7): Rankings of States by Industrial Sub-Sector Jobs – Construction

Tuesday, February 12th, 2019

Article source: ConstructConnect

There are 51 metropolitan statistical areas (CMAs) in the United States with population levels above one million each. Drawing from ConstructConnect’s data pool for those 51 cities, Table 1 ranks the Top 25 markets in America for medical facility construction starts in 2018. (Map 1 showcases the Top 20.)

Leading all cities last year was Washington, D.C., with groundbreakings on hospitals, clinics, nursing and seniors’ homes combined valued at $1.3 billion. Next in line were Cleveland ($1.1 billion), Phoenix ($883 million), Cincinnati ($858 million), Pittsburgh ($740 million), Atlanta and Orlando (tied at $736 million), Tampa-St. Petersburg ($718 million); and Houston ($708 million).

Notice the presence of a pair of cities in Ohio – i.e., Cleveland and Cincinnati – only a rung or two short of the summit in the dollar-volume listing.

(more…)

Tags: Alex Carrick, ConstructConnect, Construction industry, Construction services, Economic, Medical Facility

Comments Off on Top 25 U.S. Cities for Medical Facility Construction Starts

Wednesday, February 6th, 2019

Article source: ConstructConnect

There are 51 metropolitan statistical areas (CMAs) in the United States with population levels above one million. Drawing from ConstructConnect’s data pool for those 51 cities, Table 1 ranks the Top 25 markets in America for educational facility construction starts last year. (Map 1 showcases the Top 20.)

| Educational Facility Construction Starts |

| Top 25 Markets among Biggest U.S. Cities* |

| 2018 |

| Rank by |

|

|

|

|

|

| 2018 |

|

2017 |

2018 |

|

% Change |

| $ Value |

City / MSA |

($billions) |

|

2018/2017 |

| 1 |

New York, NY-NJ |

$3.290 |

$3.367 |

|

2.3% |

| 2 |

Dallas-Ft Worth, TX |

$2.355 |

$3.100 |

|

31.7% |

| 3 |

Los Angeles, CA |

$2.416 |

$2.626 |

|

8.7% |

| 4 |

Houston, TX |

$2.778 |

$2.592 |

|

-6.7% |

| 5 |

Seattle-Tacoma, WA |

$1.970 |

$1.560 |

|

-20.8% |

| 6 |

Chicago, IL |

$1.188 |

$1.219 |

|

2.6% |

| 7 |

Boston, MA |

$2.023 |

$1.217 |

|

-39.8% |

| 8 |

San Francisco – Oakland, CA |

$1.014 |

$1.145 |

|

13.0% |

| 9 |

Portland, OR-WA |

$0.370 |

$1.117 |

|

201.8% |

| 10 |

Philadelphia, PA |

$0.790 |

$1.090 |

|

38.0% |

| 11 |

Atlanta, GA |

$0.807 |

$0.991 |

|

22.8% |

| 12 |

Washington, DC – VA – MD – WV |

$1.279 |

$0.966 |

|

-24.5% |

| 13 |

San Diego, CA |

$0.543 |

$0.907 |

|

67.2% |

| 14 |

Baltimore, MD |

$0.917 |

$0.866 |

|

-5.6% |

| 15 |

Sacramento, CA |

$0.291 |

$0.852 |

|

193.0% |

| 16 |

Austin, TX |

$0.961 |

$0.762 |

|

-20.7% |

| 17 |

San Antonio, TX |

$1.142 |

$0.735 |

|

-35.6% |

| 18 |

Las Vegas, NV |

$0.286 |

$0.654 |

|

128.7% |

| 19 |

Orlando, FL |

$0.640 |

$0.613 |

|

-4.1% |

| 20 |

Salt Lake City, UT |

$0.660 |

$0.609 |

|

-7.7% |

| 21 |

Cleveland, OH |

$0.369 |

$0.586 |

|

59.0% |

| 22 |

Raleigh, NC |

$0.372 |

$0.574 |

|

54.3% |

| 23 |

Denver, CO |

$0.422 |

$0.573 |

|

35.8% |

| 24 |

Minneapolis – St Paul, MN – WI |

$0.843 |

$0.561 |

|

-33.4% |

| 25 |

Providence, RI-MA |

$0.306 |

$0.551 |

|

80.1% |

|

|

|

|

|

|

| *There are 51 metropolitan statistical areas (MSAs) in the U.S. with populations exceeding onemillion. |

|

|

|

|

|

| Data source and table: ConstructConnect ‘Insight’. |

|

|

|

|

|

(more…)

Tags: Alex Carrick, ConstructConnect, Construction industry, Economic, Economist, Growth, house, Housing, market, material, US

Comments Off on Top 25 U.S. Cities for School Construction Starts

Friday, February 1st, 2019

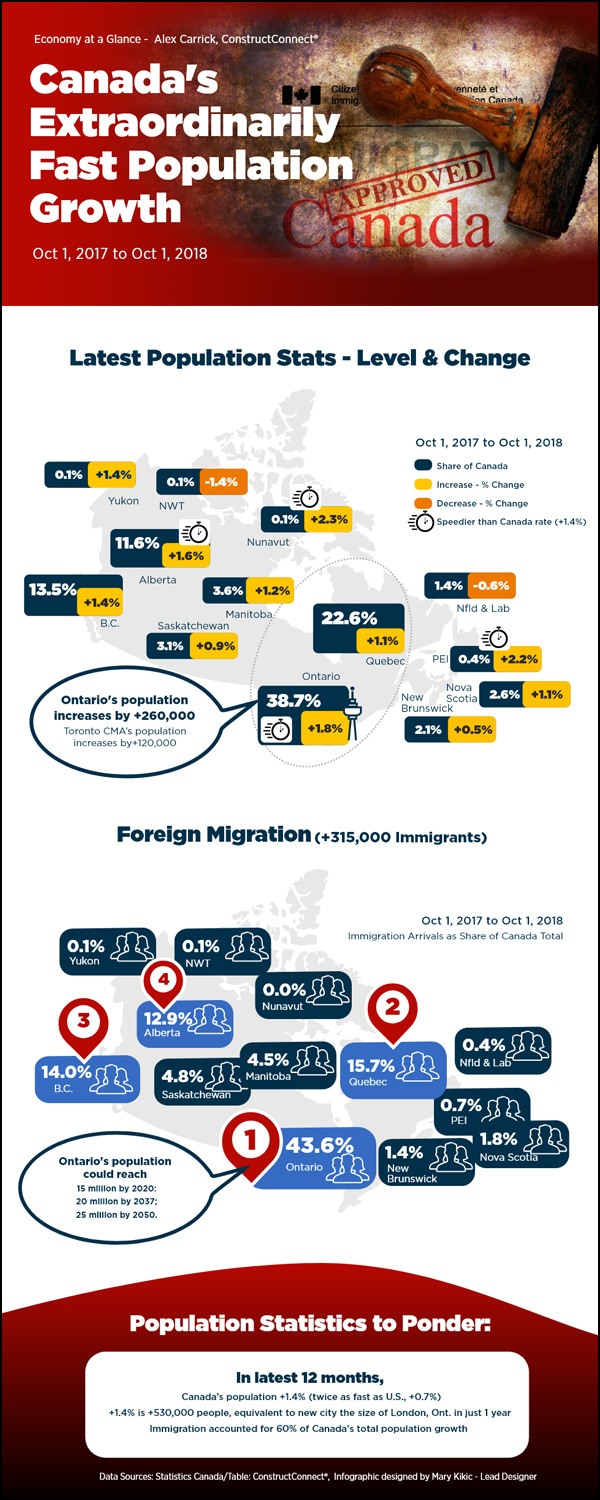

Due to its complexity, much of the subject matter concerning the economy requires detailed editorial commentary, often supported by relevant tables and graphs. This infographic looks at Canada’s extraordinarily fast population growth and the latest statistics.

At the same time, though, there are many topics (e.g., relating to demographics, housing starts, etc.) that cry out for compelling ‘short-hand’ visualizations.

Whichever path is followed, the point of the journey, almost always, is to reach a bottom line or two.

To provide additional value at its corporate blog site, ConstructConnect is now pleased to offer an ongoing series of Infographics.

These will help readers sort out the ‘big picture’ more clearly.

Click Here to view the latest infographic.

To view more infographics, Click Here

Also read the related article, “15 Bullet Points on Canada’s Extraordinarily Fast Population Growth“.

Tags: Alex Carrick, Canada, ConstructConnect, Construction industry, Construction services, Economic, Economist, population

Comments Off on Infographic: Canada’s Fast Population Growth

Friday, January 18th, 2019

Article source: ConstructConnect

Construction spending in various type-of structure categories is driven by economic circumstances within specific industrial subsectors. For example, manufacturers set the pace in industrial construction.

Good health in the leisure and hospitality sector provides the backing for new hotel and motel work. And jobs levels in information and financial services, as well as in more rapidly expanding fields of endeavor such as computer systems and design services, establish the need for additional office space and commercial tower square footage. (See, “Shifts in Office Jobs and Implications for Commercial Tower Construction.”)

This article is the second in a series of seven that examines key industrial sectors to determine where they are most prominent regionally. Rankings of state strength in each industrial subsector are based on both ‘weight’ and ‘concentration’ of relevant employment. ‘Weight’ is simply the number of jobs in the industrial subsector in each state. ‘Concentration’ is each state’s number of jobs in the subsector divided by the state’s population. In effect, it’s a ‘per capita’ figure, except that it’s expressed as number of jobs per million population.

By ‘weight’, the states with the largest populations are almost always high in the rankings. The rankings by ‘concentration’, however, often deliver a jolt of surprise or two.

(more…)

Tags: Alex Carrick, ConstructConnect, Construction industry, Construction services, Economic, Economist, employment, Growth, information sector, market, software

Comments Off on Series (3 of 7): Rankings of States by Industrial Subsector Jobs – Information Services

|

Animation, 3D Art and 3D Models")

{kind=link}